Fiserv has joined the Swift Partner Program, allowing the bank technology seller to enable connectivity to Swift’s application programming interfaces and support Swift’s Global Payment Initiative.

Swift’s GPI lets parties track payments across different banks and countries through a single source — a capability that’s considered a key cog in Swift’s real-time and cross border payment strategy.

Fiserv is attempting to make it easier for its financial institution clients to offer cross-border digital payments, or to set up digital payments in new countries.

Like many bank technology firms, Fiserv is in the midst of expanding its ability to connect banks to real-time payment networks, which will require technology upgrades to support interoperability across borders.

A group of payment technology companies including Wise, Wealthsimple, Xero Canada, Borrowell and fintech industry lobbyist Fintechs Canada have started the Choose More campaign, which is pushing for open banking.

Open banking refers to using data sharing to enable a single log in (usually a payment credential) to access financial and nonfinancial products from other companies.

Adoption of open banking in Canada is relatively low, and there isn’t a formal framework to govern open banking in Canada.

The Choose More campaign is designed to pressure faster work on data portability regulations, while educating consumers about data sharing and real-time payments, which are also delayed in Canada. Small financial institutions and credit unions are also advocating for open banking in Canada.

The first day of Nigeria Fintech Week 2023 was packed with innovative minds from across the financial sector, with eye opening insights to help push the nation’s economy forward.

The first day of Nigeria Fintech Week 2023 was packed with innovative minds from across the financial sector, with eye opening insights to help push the nation’s economy forward.

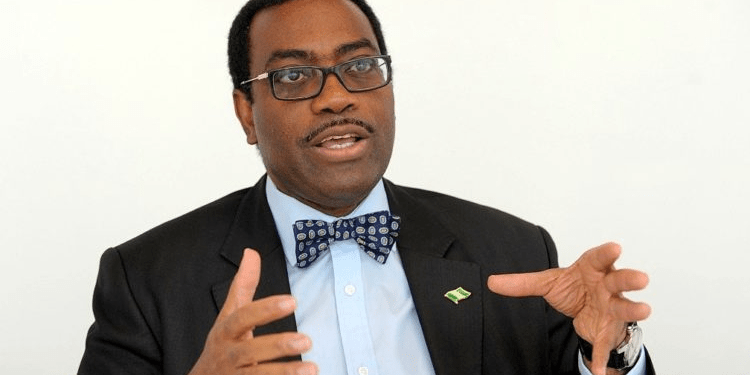

Dr. Akinwumi Adesina, the President of the African Development Bank, gave a compelling keynote address. His insights shed light on the programme’s theme “Fintech: Resilience, Innovation, & Diversification” in the fintech industry, not only in Nigeria but across the entire African continent and the global fintech arena.

Nigeria Fintech Week has evolved into a pioneering event for financial sector leaders, not just within Nigeria but on a global scale. It serves as a platform for dialogue and collaboration between industry leaders, offering a unique opportunity to explore the latest trends and developments in fintech.

“The theme for this year’s Fintech Week, ‘Resilience, Innovation, and Diversification,’ resonates particularly with the current global economic landscape,” Adesina said speaking through Lamin Barrow, the Director General of Nigeria, African Development Bank (AfDB).

Lamin Barrow, the Director General of Nigeria, African Development Bank (AfDB), representing Dr. Akinwumi Adesina at NFW 2023

“Fintech companies are grappling with the need to adapt to rapidly changing conditions, particularly in the wake of global economic downturns characterized by volatility and heightened uncertainties. These challenges are particularly evident in Nigeria and other African nations, with manifestations in macroeconomic instability, rapid forex depreciation, and rising inflation. Consequently, Africa’s GDP growth has seen a decline, estimated at 2.8% in 2022, down from 4.8% in 2021.”

Tech | Business | Economy

PODCAST

Home » Nigeria Fintech Week: Keynote Address by Dr. Akinwumi Adesina, President of the African Development Bank

Nigeria Fintech Week: Keynote Address by Dr. Akinwumi Adesina, President of the African Development Bank

Joan Aimuengheuwa by Joan Aimuengheuwa October 24, 2023

Nigeria Fintech Week: Keynote Address by Dr. Akinwumi Adesina, President of the African Development Bank

Dr. Akinwumi Adesina, President, African Development Bank

Dr. Akinwumi Adesina, President, African Development Bank

Sifax

Advertisements

The first day of Nigeria Fintech Week 2023 was packed with innovative minds from across the financial sector, with eye opening insights to help push the nation’s economy forward.

Dr. Akinwumi Adesina, the President of the African Development Bank, gave a compelling keynote address. His insights shed light on the programme’s theme “Fintech: Resilience, Innovation, & Diversification” in the fintech industry, not only in Nigeria but across the entire African continent and the global fintech arena.

Nigeria Fintech Week has evolved into a pioneering event for financial sector leaders, not just within Nigeria but on a global scale. It serves as a platform for dialogue and collaboration between industry leaders, offering a unique opportunity to explore the latest trends and developments in fintech.

Meet Dantown, the Port Harcourt-based Fintech Leveraging Cryptocurrency to Solve Payment Problems OCTOBER 25, 2023

“The theme for this year’s Fintech Week, ‘Resilience, Innovation, and Diversification,’ resonates particularly with the current global economic landscape,” Adesina said speaking through Lamin Barrow, the Director General of Nigeria, African Development Bank (AfDB).

Nigeria Fintech Week: Keynote Address by Dr. Akinwumi Adesina, President of the African Development Bank

Lamin Barrow, the Director General of Nigeria, African Development Bank (AfDB), representing Dr. Akinwumi Adesina at NFW 2023

“Fintech companies are grappling with the need to adapt to rapidly changing conditions, particularly in the wake of global economic downturns characterized by volatility and heightened uncertainties. These challenges are particularly evident in Nigeria and other African nations, with manifestations in macroeconomic instability, rapid forex depreciation, and rising inflation. Consequently, Africa’s GDP growth has seen a decline, estimated at 2.8% in 2022, down from 4.8% in 2021.”

In light of these challenges, the need for resilience through innovation and product diversification has never been more urgent. The fintech sector in Africa plays a major role in building this resilience by driving financial inclusion across the continent. “Recent studies indicate that 33% of adults in sub-Saharan Africa have mobile money accounts, the largest of any region globally.”

Mobile Money Revolution

Speaking further, Dr. Akinwumi Adesina noted that the 2022 GSMA report highlights that Africa now accounts for 621 billion registered mobile money accounts, representing 46% of the global total and approximately 70% of the world’s $1 trillion mobile money transactions in 2021. The spread of mobile money accounts has opened doors to better serve underserved populations traditionally excluded from the formal financial system.

“The COVID-19 pandemic underscored the significant role digital technologies can play in managing shocks. Continents with advanced digital financial service ecosystems were able to scale up emergency cash transfer programs, demonstrating the resilience of fintech in addressing critical societal needs.”

Fintech Beyond Banking

African fintechs extend their impact well beyond banking and payments. From healthtech solutions that make healthcare accessible with just a click, to agritech platforms connecting farms to markets and providing real-time weather forecasts, and affordable education services, innovation is driving inclusion and addressing various societal needs.

Global Investor Attraction

African fintechs’ capacity to innovate has attracted global investors. “Reports from Disrupt Africa and the International Finance Corporation reveal that there were 26 reported fintech acquisitions in Africa between June 2021 and July 2022. In 2021, 63% of tech funding in the continent, amounting to $2.7 billion, went to the fintech industry,” Dr. Akinwumi Adesina highlighted.

Nigeria’s Growth Potential

As the hub of the African fintech industry, Nigeria has seen the emergence of five of the 11 digital companies that have reached unicorn status. To witness significant growth in the fintech industry, Nigeria must further integrate technology into business activities. This necessitates domesticating the Startup Act and implementing regulatory reforms to simplify procedures for cross-border trade transactions, enhance access to finance for startups, and accelerate SME integration in e-commerce.

The African Development Bank’s Commitment

The African Development Bank strongly believes that a resilient, innovative, and diversified fintech sector is key to accelerating economic transformation in the continent. The bank is actively supporting African countries in bridging digital infrastructure and knowledge gaps, creating a conducive business environment to promote entrepreneurship and innovation in the fintech industry, and upskilling the youth to prepare them for the jobs of the future.

Since 2012, the African Development Bank has invested approximately $2 billion in 40 innovation and ICT projects across the continent. Notably, this includes $170 million in financing for the investment in digital and creative enterprises projects in Nigeria, a significant component of which is the establishment of venture capital funds to support startups in the digital creative industries.

Dr. Akinwumi Adesina’s keynote address at NFW Day 1 emphasized the key role that fintech plays in Africa’s economic development. In fostering resilience, innovation, and diversification, the fintech industry addresses economic challenges and also provides innovative solutions to improve the quality of life for people across the continent.

The African Development Bank’s commitment to this sector further emphasizes the transformative potential of fintech in Africa.

UAE banks’ gross assets jumped by 10.7% to more than AED3.9 trillion ($1.062 trillion) at the end of August 2023, compared to the previous year, the Central Bank of the UAE revealed.

The gross assets, which also include bankers’ acceptances, posted a 0.5% increase compared to AED3.8 trillion recorded at the end of July 2023.

The lenders’ total reserves at the Central Bank increased by 34.5% year-on-year to AED486.3 billion at the end of August, while gross credit went up by 5.5% to more than AED1.9 trillion.

Bank deposits reached around AED2.4 trillion in August, up by 10.9% year-on-year and 0.4% month-on-month.

Private sector bank deposits posted the biggest increase of 18% to approximately AED1.5 trillion.

Resident deposits went up by 13.7% year-on-year to AED2.19 trillion.

The UAE’s banking sector was previously forecast to post significant growth in 2022 and beyond, driven by advancements in technology and improvement in the global economy.

In its H1 2023 report, EY noted that the UAE banking sector could further benefit from the recent initiatives that have been introduced to boost the financial sector.

“The banking sector is expected to benefit further from the recent introduction of a host of regulatory measures, aimed at strengthening the country’s overall financial industry along with the Central Bank of the UAE’s vision to be among the top central banks globally in promoting monetary and financial stability…,” the report noted.

Emirates Islamic Bank’s third quarter 2023 returns were particularly impressive.

Record highs are what UAE’s leading banks are reporting with their nine-month results for 2023, with Dubai-headquartered EIB seeing a 56 per cent growth in profit to Dh1.65 billion. It was put together by higher ‘funded and non-funded income’ and which in turn reflected ‘improved business sentiment’.

In the July to September period alone, the Emirates Islamic Bank income grew 46 per cent from a year ago period to Dh1.2 billion. On the expenses side, they were up 35 per cent at the end of the nine months, given the focus to invest for future growth.

“We have seen growth across all our operating segments, including consumer, business and corporate banking segments,” said Farid Al Mulla, CEO. “The bank’s Sukuk book size reached a record Dh10 billion, marking both the highest absolute value and the highest percentage of total assets to date.”

We have seen growth across all our operating segments, including Consumer, Business and Corporate banking segments.

– Farid Al Mulla

Total assets shot up 15 per cent to Dh86 billion as customer financing grew 7 per cent to Dh52 billion. These are the headline numbers for EIB at the end of September:

Total assets increased to Dh86 billion and ‘maintaining a solid asset base’.

Customer financing topped Dh52 billion, which is 7% up from 2022.

Customer deposits came to Dh61 billion, an increased of 7% from 2022. CASA balances were at 75% of deposits.

Only a year after the 2016 Brexit referendum, the vast majority of US banks had set up their EU hubs in the German city. International school places were being block-booked ahead of relocations from the UK and property prices were rocketing.

But the French government had other ideas.

Emmanuel Macron, victorious after defeating far‑right candidate Marine Le Pen in France’s presidential elections, started courting the world’s biggest investment banks.

“Their people were texting our people photos of magnificent, historic buildings we could open trading floors in, saying they had amazing food and great infrastructure,” said the CEO of one major Wall Street bank. “They said they would cut income taxes, corporation taxes and make it easier for us to fire people. Everything they said they would do, they did.”

Six years on and while Frankfurt remains the formal EU headquarters for many banks, Paris has won the battle for talent.

Bank of America was the first of the Wall Street banks to nail its colours to the Paris mast after Brexit. It now has 600 staff in the French capital, 180 of whom work in fixed income sales and trading roles — that’s up from 20 before Brexit.

Goldman Sachs had just 17 people in Paris before Brexit — it now has 500. JPMorgan has 900 staff in its Paris office, around 600 of whom work in markets; it plans to up that to 1,000. Citigroup and Morgan Stanley are also all building in Paris.

“There are huge opportunities coming out of Paris,” said Vanessa Holtz, CEO of BofA Securities Europe SA and France country executive. “Since Brexit, the landscape has become even more dynamic and competitive. Paris has established itself as a major European financial centre and now offers a very wide spectrum of financial services.”

A talent crunch

However, Paris’s success as an EU financial centre is facing growing pains. The surge in international banks has led to a talent crunch as firms switch from relocating staff from London to hiring on the ground. Meanwhile, highly paid traders are scrambling for limited places at top international schools after moving their families from the UK.

“We’ve been moving people from London to Paris, but there are plenty of employees who have family ties in the UK who don’t want to move and that makes it more complicated, because very often we have to recruit locally and that is challenging,” said Fabio Lisanti, head of European markets at Citigroup, who moved to the French capital last year.

“There’s a big ecosystem of talent in Paris, but it’s not as liquid as London,” said Marc d’Andlau, co-head of Goldman Sachs’s Paris office. “It will happen, but a lot of people who have relocated are happy in their jobs right now.”

That talent crunch is leading to friction with French banks, which have had to battle an exodus of staff. The likes of BNP Paribas, Crédit Agricole and Societe Generale have scores of markets staff in Paris, but the incoming US firms offer bigger pay packets and have more financial firepower. That enables the them to poach some of the native banks’ best staff, frequently offering them a 30% premium and more capital, which in turn feeds through to bigger bonuses.

One head of markets at a top US bank said he had arranged to have lunch with a peer at a French rival. But when details emerged about a big hiring spree at the Wall Street lender, they suddenly cancelled. They’ve never rescheduled their lunch.

“This clearly rubs them up the wrong way,” the head of markets said. “We’re taking their best people, but so are seven of our rivals and some hedge funds. It’s driving up their costs massively.”

Hedge funds including Millennium Management, Point72 and Exodus Point have also been expanding in the French capital and that’s having an effect, too

“The arrival of hedge funds in Paris has prompted people on the ground in banks to move,” said Goldman’s d’Andlau. “That may create more movement in the job market.”

“We had to work hard on talent retention because we were the first bank to set up in Paris, and as a result we have been one of the obvious places to hire from,” added Jan Smorczewski, co-head of Emea FICC trading at Bank of America. “However, as Paris has grown into a significant hub, it has also helped attract talent.”

Paris is a key battleground that banking leaders are still trying to work out

One reason many traders are content to stay put is France’s Le régime des impatriés — commonly known as the ‘expatriate tax law’. This offers tax breaks that can see up to 30% of expats’ earnings remain tax-free and was key in luring highly paid traders to Paris.

But the benefit disappears when employees move jobs, meaning that any potential new employer has to shell out more to make up for traders’ lost earnings. Banks and lobby groups are pushing for change, Financial News reported, in a bid to allow talent to move more freely.

“We’ve hired some amazing people from domestic platforms that have really benefited from joining a platform like ours where there is more balance sheet,” said Citi’s Lisanti. “We’ve uncovered some exceptional talent, which were underperforming because of their current platform.”

While the infrastructure in Paris is well-developed, there has been some strain on the residential rental market as bankers have flocked to the French capital. Many have clustered around the well-to-do 15th and 16th arrondissements, which is pushing up prices, according to conversations with senior bankers.

Estate agent Savills said rental prices in Paris have increased just 3.6% since 2016, compared with 7.6% in London and 15.3% in New York. But demand for property is high, according to Kelcie Sellers, an associate in Savills’ world research team.

“The rental market in Paris has seen high levels of demand, particularly for prime furnished assets, with demand emanating from expats returning from Asia, London bankers, and French nationals looking for a pied-à-terre to use for a few days during the working week,” she said.

Meanwhile, senior traders and bankers relocating from the UK have also complained about the lack of places available for their children at international schools in the French capital. One school is particularly popular, senior bankers told FN — L’École Jeannine Manuel, which charges up to €28,000 a year for higher education.

“It’s becoming very hard and complicated to get in,” said one senior trader. “It’s something that needs to be looked at.”

Why Paris?

Paris became the preferred location for most major investment banks because they were being led by staff demand, senior bankers said. Many bankers or traders, unable to deal with clients in the EU after Brexit, faced the stark choice of relocating to the bloc or losing their jobs. The French capital, which is just a two-hour Eurostar journey to London, became the popular choice.

“In the immediate aftermath of Brexit, we didn’t have a grand plan to focus on France, but we wanted to increase our presence in continental Europe,” said Goldman’s d’Andlau. “But step-by-step, Paris has become the preferred location for a lot of our staff over other cities, so that drove some of our thinking. The pro-business agenda under President Macron was also very helpful.”

“The biggest driver for us choosing Paris was access to talent, and the ability to more easily persuade people to move from London than to other European cities,” added Citigroup’s Lisanti. “People are now permanently relocating, but the Eurostar and ease of access to London definitely has a bearing on people’s willingness to move.”

Paris has already seen an influx of bankers bringing in big pay packets. The European Banking Authority said in its latest EBA Report on High Earners that there were 371 bankers earning more than €1m in France in 2021; this was up from 226 a year earlier.

“It was a move born out of necessity, but one that has turned into a real competitive advantage,” said Jim DeMare, president of global markets at Bank of America, about its EU hub. “We hear that from our clients. We see it in our flows.”

Building up

After the initial flood of Brexit relocations, banks are now focused on building out their operations on the ground as they get more established.

Jean-Charles Simon, chief executive of Paris Europlace, which develops and promotes the French financial sector internationally, said France is now looking beyond front office jobs. It is also hoping to attract banks from emerging markets as well as the US, Canada and other countries.

“The biggest international banks are continuing to expand their workforce, but I think we have the potential to continue to grow in financial services in different kinds of activities and jobs,” he said.

Citigroup is in the process of opening a new trading floor in its Paris office that will house 80-90 people in addition to its current space, which contains 130 staff. It plans to end the year with around 170 employees in its markets business and will expand to 250 over the next couple of years, Lisanti said.

It is now considering revamping its internship programme in Paris to mirror its London scheme. Students would then come in for nine weeks over the summer, rather than for an extended period as per the French system.

“We are growing from within in a tight labour market and this means recruiting from entry level,” said Lisanti. “The summer internship allows us to hire international students, rather than relying on French‑style internships that tend to attract only students from French universities.”

Bank of America is also likely to expand into other areas, Holtz said.

“We plan to build on our success in Paris and continue to offer our global connectivity to clients in France and the EU more and more products, services and counsel to help them meet their ever-evolving needs in France, the EU and around the world,” she said.

The French expat community

For all the growing pains around France as a financial centre since Brexit, senior bankers said that it has developed from a relative backwater for international banks into a place where employees are choosing to be based for the long-term.

“If you move to Paris, you are no longer moving to an office of 20 people — it’s a chance to have a career that simply wasn’t there before Brexit when it would have been seen as a hardship posting,” said Lisanti. “People can see it’s a growing office and a little bit more entrepreneurial. Our people are moving with their families, so it’s a community.”

Banks want to see their Paris offices less as French outposts and more as European hubs with a multitude of backgrounds and nationalities, bankers said.

“Before Brexit, it could be tough to convince people to move to Paris, because they felt removed from Goldman’s main business in Europe,” added Goldman’s d’Andlau. “That has changed and people are embracing the new careers they can have in France. We have 26 nationalities in Paris and people are now happy to be here.”

Britain on Tuesday scrapped a decade-old cap on banker bonuses inherited from the European Union, signalling a clear divergence in post-Brexit financial rules from the 27-country bloc it left in 2020.

Britain was outvoted in the EU when the cap was introduced in 2014 to try to prevent the kind of behaviour that led to the global financial crisis of 2008 and its accompanying taxpayer bailouts of lenders.

The move to ditch the cap drew criticism from trade unions and campaigners on Tuesday, who dubbed it inappropriate at a time when many households were struggling in a cost of living crisis.

Most bankers affected by the cap are based in London, and the Bank of England (BoE) has long said the cap, which limits bonuses to twice basic pay if shareholders approve, has simply led to higher fixed salaries to circumvent it.

The BoE and Financial Conduct Authority proposed scrapping the cap in a public consultation earlier this year, and its abolition was confirmed in final policy published on Tuesday.

Both regulators have a remit to aid the competitiveness of London as a global financial centre as it competes with New York, where there are no bonus caps.

Allowing bankers to implement the change earlier than originally proposed will also help them meet their goal.

In a joint statement, the regulators said the changes would enter force from Oct. 31, earlier than the original 2024 proposed start date.

“We support the removal of the bonus cap, which will ensure the financial services industry is globally competitive and make the UK a more attractive place to work for international professionals,” banking industry body UK Finance said.

GRADUAL SHIFT FROM CAP

The change is still probably too late for some banks to adapt their systems in time for this year’s bonus allocations that will be paid in early 2024.

In any case, bonuses may not rise for bankers on a high basic salary that contractually cannot be reduced, as banks try to avoid allegations of adding to inflationary pressures.

A source at one multinational bank, who declined to be named, said it was too early to say if this year’s bonus round would be affected, adding that while the change was disruptive it could help attract talent from the United States and Asia.

The regulators said companies had full flexibility over when or if they changed pay structures.

“What is more likely is that the shift away from capped bonuses will evolve gradually,” said Suzanne Horne, a partner at Paul Hastings law firm.

Other curbs on bonuses remain, such as requiring 40% to be deferred over at least four years, with half the bonus paid in shares, making it easier for regulators to claw back awards if any misconduct emerges.

The TUC confederation of labour unions said the decision to scrap the bonus cap was “obscene”.

“At a time when millions up and down the country are struggling to make ends meet – this is an insult to working people,” TUC General Secretary Paul Nowak said in a statement.

Positive Money, a group that campaigns for a fair financial system, called the policy a “risky move” that prioritised banks over public wellbeing.

Law firm Linklaters said scrapping the cap puts Britain back into line with the rest of the world, apart from the EU, but it would continue to apply to staff working at EU banks in London who are regulated under the bloc’s rules.

World fintech and banking industry stakeholders will converge in London, United Kingdom (UK) for this year’s edition of the Global Reputation Forum (GRF)/Reputable Banks and Fintech Awards & Conferences (RBFA), bringing together experts from both the financial and technology sectors 8-9 December, 2023.

The quintessentially British London Marriott County Hall will be venue to the annual event which provides a platform for fintech startups and established banking institutions to showcase their latest innovations.

Participating institutions and personalities get to witness firsthand how technology is transforming traditional banking services, from digital payments and lending to robo-advisors and blockchain-based solutions.

Besides its objectives of showcase of innovation, regulatory insights, knowledge sharing, networking, market trends and predictions, GRF aims to foster collaborations between fintech startups and traditional banks in an increasingly developing industry trend.

The Reputable Banks and Fintech Awards/Conference is an initiative of Reputation Poll International (RPI), a leading global management firm known for listing the 100 Most Reputable People on Earth and Most Reputable Bank CEOs.

According to the organizers, RBFA will create an environment where these two worlds can meet and explore opportunities for collaboration, which can lead to mutually beneficial partnerships.

Beldina Auma, RBFA Co-Chair Screening Committee and former Chair African Society for the World Bank and IMF, said: “Attendees have the opportunity to learn from thought leaders, exchange ideas, and form valuable connections that can lead to collaborations and partnerships”.

“As fintech and banking industries are subject to ever-evolving regulations, GRF will include sessions dedicated to discussing compliance and regulatory changes. This is crucial for ensuring that innovative financial solutions remain in compliance with legal requirements”.

“GRF will offer a glimpse into current market trends and future predictions. Experts analyze market dynamics, consumer behavior, and emerging technologies, helping attendees make informed decisions and adapt their strategies accordingly”, Dr. Rex Idaminabo said.

Auma explained that Reputable Banks and Fintech Awards/Conference is designed to acknowledge rapid expansion, integration, accelerated growth and reforms of Africa’s banking and financial sector.

Some of the Speakers/Panelists for the 2023 edition include: Baroness Verma, Yvonne Thompson CBE, Lord JD Waverly and Franklin Amoo.

Baroness Verma is a Member of the House of Lords, UK. She was spokesperson for Cabinet Office International Development, Women and equalities and Business Innovation and Skills.

Lord JD Waverly is a Member of the House of Lords. He serves also as Co-chair: Trade and Investment All Party Parliament Group and the Founder and Chairman of the GoGlobal Trade.

Franklin Amoo is a member of the United States’ President’s Advisory Council on the East of Doing Business in Africa. He is also Managing Partner, Baylis Emerging Markets and Head, African Private Equity.

Yvonne Thompson CBE is the Founder/President of WinTrade Global Network and Deputy Lieutenant for Greater London.

Big banks in Britain are preparing for any future escalation of Western sanctions on China and have shared their “scenario planning” with the British and U.S. governments, a senior banking official has told Reuters.

The project involves sharing lessons learned from other sanctions frameworks, including those on Russia, and discussions about the effect any measures imposed on China might have, Neil Whiley, director of sanctions at lobby group UK Finance, said.

After many companies were wrongfooted by the speed and breadth of prohibitions on Russia, banks are drawing up contingency plans in case geopolitical tensions between the West and China escalate, seven finance industry sources said. They did not expect any imminent changes to sanctions.

The work by UK Finance – which represents around 300 firms, including HSBC (HSBA.L), Barclays (BARC.L) and JPMorgan (JPM.N) – examines the transparency of asset ownership and control and how easily Chinese products can be traced, Whiley said.

It also focuses on the extent of commercial ties between the West and China across industries, including supply chains in high-risk sectors like technology, and attempts to highlight measures that might backfire if applied to China.

The work has been carried out against a backdrop of tensions between the West and China over the status of Taiwan, which Beijing claims, growing export controls, accusations of Chinese spying and a security crackdown by Beijing on companies.

UK Finance convened fortnightly meetings of big British and overseas banks over several months, Whiley said, before drawing up a draft document that runs to tens of thousands of words. Reuters was not able to review the document.

The draft was completed in August and shared with Western government contacts in recent weeks, he said.

The U.S. Treasury Department, which runs the Office of Financial Sanctions Implementation, Britain’s Foreign Office and Barclays did not respond to requests for comment. JPMorgan declined to comment.

TRACING RISKS

The preparations have been driven in part by the unprecedented sanctions slapped on Russia following its full-scale invasion of Ukraine, which left some companies struggling to get assets out of the country or exit positions.

One of the bankers said sanctions on Russia had “removed naivety” among businesses and prompted the industry to think more deeply about China risks.

Communications between officials from the United States and China have increased in recent months, thawing frosty relations somewhat ahead of a meeting between Chinese President Xi Jinping and U.S. President Joe Biden next month.

China, the world’s second-largest economy, remains central to Western supply chains. The European Union’s trade deficit with China, for example, widened to $276.6 billion in 2022 from $208.4 billion a year earlier, Chinese customs data show.

British finance also has close ties with China. Two of the country’s biggest banks – HSBC and Standard Chartered – make most of their profits in Asia, forcing them to straddle the geopolitical faultlines.

HSBC and Standard Chartered declined to comment.

SURGE IN CALLS

Whiley said the UK Finance project was designed to be part of industry-wide “horizon-scanning” to assess potential risks across multiple countries, in line with regulatory guidance, and did not reflect expectations or requests for more sanctions.

Nonetheless, financial firms are alive to the risks.

Another banker, who works for a lender with a presence in Asia, said the bank’s board was planning for more strains between China and Taiwan and likely consequences for financial markets, including currency and equity reactions.

Lloyd’s of London underwriters are among insurers that have raised rates and cut cover for risks involving Taiwan as concerns grow about possible military action by China, Reuters exclusively reported in August.

Against that background, four lawyers in London reported a surge in calls from financial clients seeking guidance on China, from sanctions compliance and risk assessment through to how to deal with any investigations or enforcement.

Demand for advice was so keen that one lawyer, who declined to be identified, said his firm last month held its first client-only seminar on Russia, China and how geopolitics were shaping sanctions and compliance.

“Companies will … want to make sure that for long-term engagements with Chinese entities, they have robust sanctions provisions in their contracts and agreements,” said Leigh Hansson, a London and Washington-based lawyer at Reed Smith.

Banks’ concerns are being driven partly by the robust U.S.-steered approach to the semi-conductor and technology industry and foreign policy discussions, lawyers said.

The Biden administration has curbed chip exports to China to deny Beijing access to advanced technology that could further military advancements or human rights abuses. China hit back with accusations of economic coercion.

One lawyer said he did not expect any repeat of the Russia response and for “commercial reality” to enter foreign policy decision-making in relation to China.

“(Any sanctions) will be very much targeted at specific companies, specific products and services,” the lawyer said.

Despite having around 28 per cent of the world’s Muslim population, Africa’s Shariah compliant banking assets make up only around two per cent of global Islamic banking assets, Moody’s Investors Service has said.

A report issued Thursday by the rating agency, stated that African Islamic banks face obstacles to growth, including high level of competition from conventional banks in some countries and a lack of product awareness in some other jurisdictions.

While the industry’s na- scent legal and regulatory landscape has been among the constraints, there is noticeable progress now being made in jurisdictions such as Morocco, Nigeria and across the West African Economic and Monetary Union (WAEMU), the report said.

“The Islamic banking industry remains underdeveloped in Africa as product awareness and sector competitiveness lag domestic conventional peers in some countries. However, legal, regulatory and tax frameworks are progressing well in some jurisdictions,’’ said Mik Kabeya, Vice President, Analyst at Moody’s.